- Browse Category

Subjects

We Begin at the EndLearn More

We Begin at the EndLearn More - Choice Picks

- Top 100 Free Books

- Blog

- Recently Added

- Submit your eBook

- Browse Category

We Begin at the EndLearn More

- Choice Picks

- Top 100 Free Books

- Blog

- Recently Added

- Submit your eBook

Elements of Stochastic Modelling

2020-05-26 11:15:12

This is the expanded second edition of a successful textbook that provides a broad introduction to important areas of stochastic modelling. The original text was developed from lecture notes for a one-semester course for third-year science and actuar...

Read more

This is the expanded second edition of a successful textbook that provides a broad introduction to important areas of stochastic modelling. The original text was developed from lecture notes for a one-semester course for third-year science and actuarial students at the University of Melbourne. It reviewed the basics of probability theory and then covered the following topics: Markov chains, Markov decision processes, jump Markov processes, elements of queueing theory, basic renewal theory, elements of time series and simulation. The present edition adds new chapters on elements of stochastic calculus and introductory mathematical finance that logically complement the topics chosen for the first edition. This makes the book suitable for a larger variety of university courses presenting the fundamentals of modern stochastic modelling. Instead of rigorous proofs we often give only sketches of the arguments, with indications as to why a particular result holds and also how it is related to other results, and illustrate them by examples. Wherever possible, the book includes references to more specialised texts on respective topics that contain both proofs and more advanced material.

Less

Compare Prices

| Store | Availability | Book Format | Condition | Price |

|---|---|---|---|---|

| eBooks.com | In Stock | Buy GBP 34.58 | ||

| Indigo Books & Music | In Stock | Buy CAD 153.50 |

Available Discount

No Discount available

Related Books

View All

Claims Reserving in General Insurance

Excel Basics to Blackbelt

How to Open & Operate a Financially Successful Personal Chef Business

Exclusionary Practices

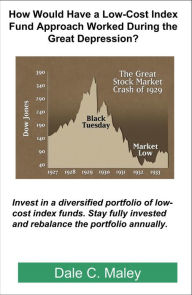

How Would Have a Low-Cost Index Fund Approach Worked During the Great Depression?

Empowering Leadership of Tomorrow

Productivity Accounting

Herding Cats

Equitable Principles of Maritime Boundary Delimitation

State and Local Financial Instruments

Termites of the State

Religion and Contemporary Management

Theory and Reality in Financial Economics

Principles of Financial Economics

Theory and Empirical Research in Social Entrepreneurship

Motives and Effectiveness of Forex Interventions

Graduate Migration and Regional Development

A Dictionary of the Internet

Teaching Entrepreneurship

A Beginner's Guide to Mobile Marketing

The Cambridge Economic History of Modern Britain

Handbook on the Economics of Professional Football

International Exchange of Information in Tax Matters

Oil, Democracy, and Development in Africa

Water Ecosystem Services

Settings

Reflow text when sidebars are open.