- Browse Category

Subjects

We Begin at the EndLearn More

We Begin at the EndLearn More - Choice Picks

- Top 100 Free Books

- Blog

- Recently Added

- Submit your eBook

- Browse Category

We Begin at the EndLearn More

- Choice Picks

- Top 100 Free Books

- Blog

- Recently Added

- Submit your eBook

Introduction to Malliavin Calculus

2020-03-20 15:44:07

This textbook offers a compact introductory course on Malliavin calculus, an active and powerful area of research. It covers recent applications, including density formulas, regularity of probability laws, central and non-central limit theorems for G...

Read more

This textbook offers a compact introductory course on Malliavin calculus, an active and powerful area of research. It covers recent applications, including density formulas, regularity of probability laws, central and non-central limit theorems for Gaussian functionals, convergence of densities and non-central limit theorems for the local time of Brownian motion. The book also includes a self-contained presentation of Brownian motion and stochastic calculus, as well as Lévy processes and stochastic calculus for jump processes. Accessible to non-experts, the book can be used by graduate students and researchers to develop their mastery of the core techniques necessary for further study.

Less

Compare Prices

| Store | Availability | Book Format | Condition | Price |

|---|---|---|---|---|

| eBooks.com | In Stock | Buy GBP 19.99 | ||

| Indigo Books & Music | In Stock | Buy CAD 126.95 |

Available Discount

No Discount available

Related Books

View All

How to Open & Operate a Financially Successful Personal Chef Business

State and Local Financial Instruments

Excel Basics to Blackbelt

Termites of the State

Handbook on the Economics of Professional Football

Theory and Empirical Research in Social Entrepreneurship

Theory and Reality in Financial Economics

Equitable Principles of Maritime Boundary Delimitation

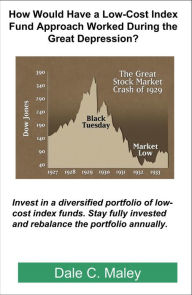

How Would Have a Low-Cost Index Fund Approach Worked During the Great Depression?

Claims Reserving in General Insurance

Exclusionary Practices

A Beginner's Guide to Mobile Marketing

Water Ecosystem Services

Motives and Effectiveness of Forex Interventions

Principles of Financial Economics

Graduate Migration and Regional Development

The Cambridge Economic History of Modern Britain

Oil, Democracy, and Development in Africa

International Exchange of Information in Tax Matters

Productivity Accounting

Empowering Leadership of Tomorrow

Religion and Contemporary Management

Herding Cats

A Dictionary of the Internet

Teaching Entrepreneurship

Settings

Reflow text when sidebars are open.